Capital One has finalized an agreement to acquire the technology infrastructure, supplier relationships, and a specialized workforce of 150 employees from the travel-tech firm Hopper, marking a significant shift in the bank’s strategy to internalize its travel ecosystem. The deal, which was confirmed by a Capital One spokesperson on Tuesday, represents a transition from a collaborative partnership to a direct ownership model for the technology that powers Capital One Travel. This move allows the financial giant to gain full control over the customer experience, backend licensing, and servicing contracts that were previously managed through Hopper’s "Hopper Cloud" B2B initiative.

The announcement follows months of industry speculation. In November, reports surfaced suggesting that Capital One intended to purchase the installed software from Hopper and integrate the personnel responsible for its development. While both companies remained silent at the time, the formal confirmation signals the end of a four-year development cycle where Hopper acted as the primary engine for Capital One’s travel portal. By bringing these capabilities in-house, Capital One is positioning itself to compete more aggressively with established premium travel players like American Express and JPMorgan Chase.

The Strategic Shift Toward Internalized Travel Ecosystems

The acquisition of Hopper’s infrastructure and talent is a clear indication of Capital One’s ambition to move beyond being a mere financial intermediary. For years, major credit card issuers relied on third-party online travel agencies (OTAs) or technology providers to fulfill travel bookings for their cardholders. However, as travel has become a central pillar of the "premium" credit card market, the limitations of third-party dependencies have become more apparent.

By acquiring the technology and the 150 employees who built it, Capital One is securing the intellectual property and human capital necessary to iterate on its platform without external bottlenecks. The transition includes the acquisition of crucial licenses and servicing contracts, which will allow Capital One to establish direct relationships with airlines, hotel chains, and car rental agencies. This direct-to-supplier model is expected to improve the bank’s margins and allow for more bespoke loyalty offerings that are not restricted by a middleman’s technical architecture.

Hopper, in a parallel statement, framed the deal as a natural evolution of their partnership. The company noted that as Capital One Travel scales, bringing the portal in-house ensures continuity and allows the bank to leverage the foundational work already completed. The 150 employees transitioning to Capital One include engineers, product managers, and support staff who have been deeply embedded in the Capital One Travel project since its inception.

A Chronology of the Capital One and Hopper Partnership

The relationship between the two companies began in earnest in early 2021, a period when the travel industry was grappling with the fallout of the global pandemic but preparing for a massive rebound in consumer demand.

- March 2021: Capital One announced a $170 million Series F funding round for Hopper, which valued the travel startup at approximately $3.5 billion. This investment was accompanied by the news that Hopper would power the new Capital One Travel portal.

- Late 2021: Capital One Travel officially launched, featuring Hopper-integrated tools such as price prediction, price dropping, and "cancel for any reason" flexibility. These features were central to the marketing of the Capital One Venture X card, which launched around the same time to compete in the high-end travel segment.

- 2022: The partnership deepened as Hopper Cloud—the company’s B2B arm—expanded. Capital One became the flagship client for Hopper’s fintech products, which used data science to manage the financial risks associated with price volatility in the travel sector.

- November 2023: Initial reports emerged from industry insiders suggesting that Capital One was moving to acquire the specific software stack it was using from Hopper, alongside the core team dedicated to the account.

- May 2024: Capital One and Hopper officially confirm the "payout" and the transition of 150 employees, signaling the formal internalization of the platform.

Data and Market Context: The Stakes of the Premium Travel War

The decision to bring travel operations in-house is backed by compelling data regarding consumer spending habits. Travel remains one of the largest spending categories for high-net-worth credit card users. According to industry reports, travel-related spending on premium credit cards saw a 15% year-over-year increase in 2023, even as other discretionary categories cooled due to inflation.

For Capital One, the Venture X card has been a significant driver of new, younger, and high-spending customers. Data suggests that millennials and Gen Z travelers are more likely to use integrated booking portals if they offer unique fintech protections, such as "Price Freeze" or "Flight Disruption Guarantee." By owning the technology that powers these features, Capital One can refine the algorithms behind them using its own proprietary customer data, rather than relying on Hopper’s generalized datasets.

Furthermore, the competitive landscape has forced this evolution. JPMorgan Chase acquired the luxury travel agency Frosch in 2022 and launched its own travel brand, Chase Travel, aiming to process $15 billion in bookings by 2025. American Express has long owned its own travel agency and the Fine Hotels + Resorts program. For Capital One to maintain its trajectory, the transition from a "partner-led" model to an "owner-operator" model was viewed by analysts as a necessary step for long-term scalability.

Financial Implications and the "Acqui-hire" Strategy

While the specific financial terms of the "payout" were not disclosed, the transaction functions as a hybrid between a technology acquisition and an "acqui-hire." In the tech world, an acqui-hire is often used to secure specialized talent in a competitive market. By bringing over 150 employees, Capital One avoids the multi-year recruitment and training cycle that would have been required to build a travel-tech division from scratch.

For Hopper, the deal provides a significant cash infusion and allows the company to focus on its B2C app and other B2B partnerships under Hopper Cloud. Hopper has recently faced pressure to reach profitability after years of rapid, venture-backed growth. Offloading the specific infrastructure and personnel dedicated to Capital One allows Hopper to lean out its operations while still maintaining a commercial relationship with one of the world’s largest financial institutions.

The move also impacts the supplier side of the business. Previously, Hopper acted as the Merchant of Record for many transactions on Capital One Travel. By taking over the supplier relationships and servicing contracts, Capital One becomes the primary negotiator. This shift gives the bank more leverage when negotiating exclusive rates or "member-only" benefits with major hotel groups like Marriott, Hilton, or Hyatt, and airlines such as United and American.

Industry Reactions and Analyst Perspectives

Market analysts suggest that this move is a defensive and offensive play. Defensively, it protects Capital One from any potential instability or strategic pivots at Hopper. If Hopper were to be acquired by a competitor or face financial headwinds, Capital One’s core travel offering could have been at risk. Offensively, it allows for a more seamless integration with Capital One’s broader financial ecosystem.

"The goal for these banks is to create a ‘sticky’ ecosystem," says one travel industry consultant. "If a customer books their flight, stays in a hotel, and manages their credit card rewards all in one app—and that experience is flawless—they are much less likely to churn to a competitor. By owning the tech stack, Capital One can ensure that the ‘flawless’ part of that equation is under their direct control."

The transition of 150 employees is also seen as a vote of confidence in the specific product culture Hopper built. These employees are not just general engineers; they are experts in "travel fintech"—a niche field that combines predictive analytics with travel booking. Their integration into Capital One suggests the bank intends to keep innovating in areas like automated rebooking and real-time price hedging.

Future Outlook: The Evolution of Capital One Travel

As Capital One Travel moves in-house, the immediate focus will be on the continuity of service. The spokesperson noted that the transition is designed to ensure that cardholders see no disruption in their booking experience. In the medium term, however, users can expect a more deeply integrated experience.

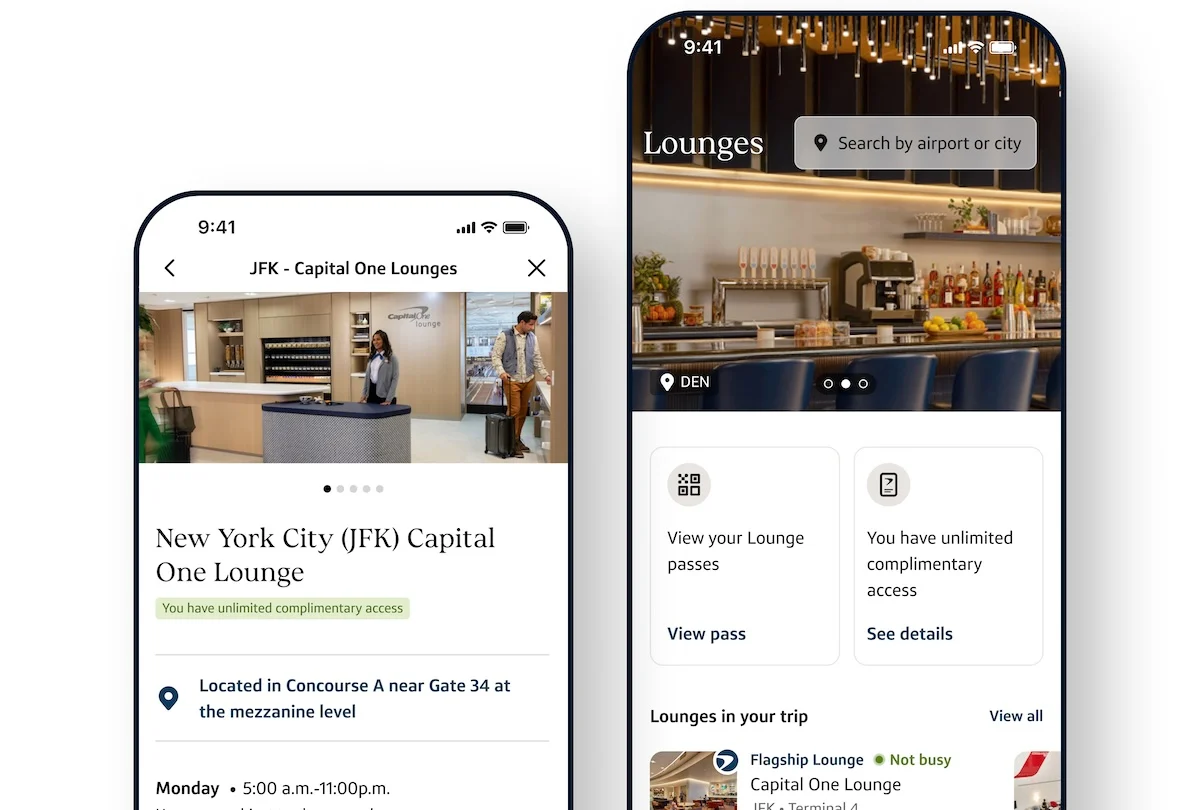

One potential area of expansion is the integration of Capital One’s physical assets, such as its growing network of airport lounges. With direct control over the booking technology, the bank could theoretically offer dynamic lounge access or "bundle" travel packages that include lounge entry, expedited security, and premium seating in a way that would have been technically complex under a third-party arrangement.

Furthermore, the move signals a broader trend in the fintech world: the "unbundling" and then "rebundling" of services. While specialized startups like Hopper paved the way for innovation, the massive scale and capital of traditional banks are now being used to consolidate those innovations into "super-apps."

Capital One’s decision to bring its travel technology in-house is a landmark moment in the intersection of finance and travel. It underscores the reality that for modern credit card issuers, travel is no longer a peripheral perk—it is a core product that requires direct ownership, specialized talent, and a robust, proprietary technological foundation. As the 150 employees transition and the infrastructure is integrated, the industry will be watching closely to see how this newfound autonomy translates into market share in the high-stakes world of premium travel.