Omaha, Nebraska – Berkshire Hathaway, the sprawling conglomerate led by Warren Buffett and now helmed by CEO Greg Abel, announced Thursday a significant dual move aimed at bolstering investor confidence: the resumption of its share repurchase program for the first time since the second quarter of 2024, coupled with a substantial personal investment by Abel himself. The company disclosed that it began buying back its Class A and Class B shares on Wednesday, a strategic decision made after Abel consulted with Chairman Warren Buffett, based on their shared assessment that Berkshire’s stock was trading below its intrinsic value. Simultaneously, Abel purchased $15 million worth of Berkshire stock, an amount equivalent to his after-tax annual salary, and pledged to continue this personal investment annually, signaling profound alignment with the company’s shareholders.

The news, which saw Berkshire B shares add 1% in early trading Thursday, arrives at a critical juncture for the Omaha-based giant. Just days prior, Berkshire Hathaway reported a nearly 30% decline in its operating earnings for the fourth quarter of 2025, largely attributed to softness within its vast insurance businesses. This earnings report, combined with broader market pressures, had seen the company’s shares retreat 10% from their record high achieved in May. Against this backdrop, the twin announcements serve as a powerful statement of belief in Berkshire’s underlying value and future prospects from both its corporate leadership and its chief executive.

A Return to Value-Driven Capital Allocation

Berkshire Hathaway’s approach to share repurchases has long been a cornerstone of its capital allocation strategy, deeply rooted in Warren Buffett’s philosophy. Unlike many companies that implement routine buyback programs, Berkshire’s policy is explicitly tied to intrinsic value. The company repurchases shares only when the chief executive, in consultation with the chairman, believes the stock is trading at a discount to its true worth. This disciplined, value-oriented approach ensures that repurchases genuinely benefit continuing shareholders by reducing the share count at an advantageous price, thereby increasing their ownership stake in the company’s underlying assets and earnings power.

Historically, Berkshire’s buyback policy underwent a significant evolution in 2018. Prior to that, repurchases were only authorized if shares traded at or below 1.2 times book value. Recognizing that book value might not always accurately reflect intrinsic value, especially given the increasing weight of non-financial assets and intangible values within its portfolio, Buffett and his long-time partner Charlie Munger revised the policy. The new framework granted more discretion to management, allowing buybacks whenever both Buffett and Munger (and now, Abel) agreed that the price was below intrinsic value. This shift empowered Berkshire to become a more aggressive repurchaser of its own stock, deploying billions of dollars when market conditions presented opportunities. For instance, in the years following the 2018 policy change, Berkshire deployed tens of billions of dollars in share repurchases, particularly during periods of market volatility or when its stock lagged. The last reported buyback activity was in the second quarter of 2024, making this week’s resumption a notable event that breaks a multi-quarter hiatus.

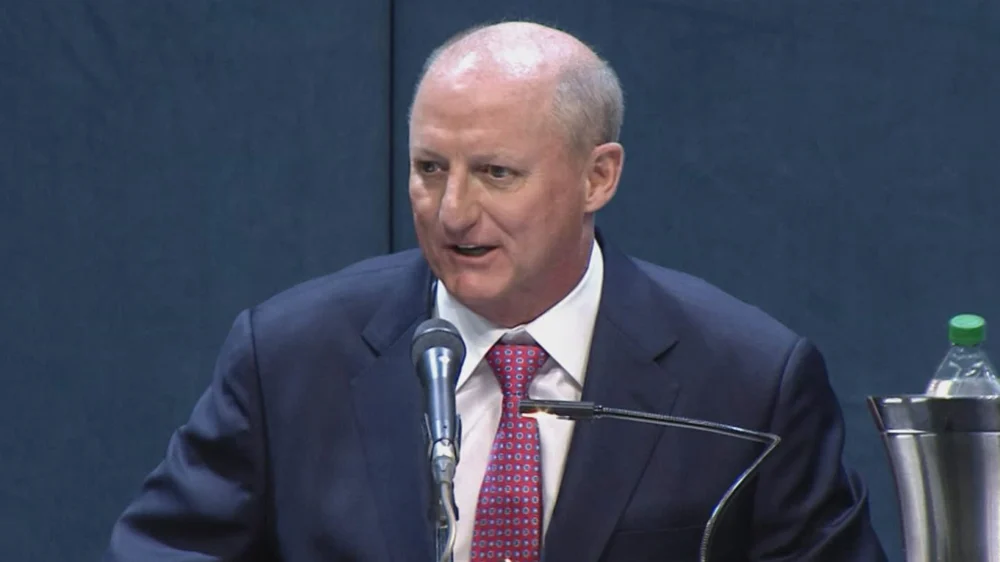

Greg Abel’s confirmation that he "absolutely talked to Warren" regarding the buyback decision underscores the continuity of this value-centric approach. "So how I approached it was, obviously looking at the value, having a view of intrinsic value, consulted with Warren relative to the value and the timing," Abel told CNBC’s "Squawk Box." This consultation is not merely a formality; it signifies the ongoing partnership and shared intellectual capital between the iconic investor and his chosen successor. For investors, it offers reassurance that the bedrock principles of Berkshire’s financial management remain firmly in place, even as the operational leadership transitions.

Transparency in Transition: Communicating with Shareholders

Abel also shed light on the company’s decision to publicly disclose the initiation of the repurchase plan, a practice not typically followed for every buyback. "We felt it was important to communicate to our shareholders, our partners, our owners, with the transition of leadership," he explained. This transparency is particularly salient in the context of a leadership handover at a company as closely watched and ideologically driven as Berkshire. It sends a clear message that the new leadership is proactive, confident in the company’s valuation, and committed to open communication with its vast shareholder base.

The decision to buy back shares follows a period of market pressure on Berkshire. The conglomerate’s diverse portfolio, encompassing everything from insurance (GEICO, General Re, National Indemnity) and energy (Berkshire Hathaway Energy) to manufacturing (Precision Castparts, Marmon), retail (See’s Candies, Dairy Queen), and railroads (BNSF), typically provides stability. However, the reported nearly 30% decline in Q4 2025 operating earnings indicates specific headwinds, particularly within the insurance segment. While specific details were not elaborated in the initial article, such weakness can stem from various factors including elevated catastrophe losses, adverse prior-year reserve development, increased competition impacting underwriting margins, or unfavorable investment income trends within the insurance float. A subsequent stock decline of 10% from its peak would naturally make the shares appear more attractive to a value investor, triggering the conditions for a repurchase.

Greg Abel’s Personal Commitment: Deepening "Skin in the Game"

Beyond the corporate action, Greg Abel’s personal purchase of $15 million in Berkshire stock stands as a powerful testament to his belief in the company he now leads. This amount, directly equating to his after-tax annual salary, is a deliberate and visible act of alignment. Abel, who is 62, has pledged to continue using his full salary to purchase Berkshire shares every year, a commitment he hopes to maintain for "20 years" at the helm.

This level of personal investment directly addresses a narrative that has occasionally surfaced among some investors regarding "skin in the game" for Buffett’s successor. Warren Buffett’s legendary status is inextricably linked to his ownership stake in Berkshire Hathaway, which represents roughly 99.5% of his net worth (excluding charitable giving) and accounts for about 37.5% of Berkshire’s Class A shares. This immense personal alignment has long been a source of comfort and confidence for Berkshire shareholders, ensuring that Buffett’s interests were always perfectly synchronized with theirs.

While Abel, a long-time Berkshire executive who previously oversaw the company’s non-insurance operations, already owned a significant stake of $164.4 million worth of Berkshire stock prior to this latest purchase (according to FactSet), his new action significantly deepens that commitment. It is a proactive move to bridge any perceived gap in alignment with the founder. "Absolute alignment with our shareholders, our partners, our owners, is critical," Abel articulated. "I already have some shares, but the goal was to continue to demonstrate alignment with them… As the CEO, I absolutely, obviously, believe in Berkshire. with the transition from Warren, and I inherited a company that has an incredible foundation."

This commitment reinforces the messaging from Abel’s first annual shareholder letter, released over the weekend. In that letter, he explicitly vowed to maintain Berkshire’s cherished culture of financial conservatism and disciplined investing "into perpetuity." His personal stock purchases and the strategic corporate buyback are not merely financial transactions; they are symbolic actions designed to demonstrate that these vows are backed by tangible commitment and confidence.

Broader Implications and Investor Sentiment

The combined announcements carry significant implications for investor sentiment and the future trajectory of Berkshire Hathaway under Abel’s leadership.

Firstly, they signal a seamless transition of the core capital allocation philosophy. The fact that the buyback was initiated only after consultation with Warren Buffett confirms that the foundational principles of value investing remain paramount. This continuity is vital for a company with Berkshire’s unique culture and long-term investment horizon.

Secondly, Abel’s personal investment acts as a strong vote of confidence from the company’s highest executive. In an environment where executive compensation structures are often scrutinized, Abel’s decision to reinvest his entire annual salary back into the company’s stock speaks volumes. It’s a powerful endorsement that his financial future is directly tied to the success of Berkshire Hathaway, aligning his personal prosperity with that of every shareholder. This proactive move is likely to be met with approval from institutional investors and retail shareholders alike, who value leadership that genuinely believes in the company’s prospects.

Thirdly, the timing of these actions is strategic. Following a dip in operating earnings and a corresponding decline in share price, the company and its CEO are effectively "buying the dip." This demonstrates a belief that the recent setbacks are temporary or do not fundamentally impair Berkshire’s intrinsic value. It suggests management views the current market valuation as an attractive entry point, either for corporate capital deployment or personal investment.

Finally, these moves underscore the challenge and opportunity for Berkshire Hathaway in a post-Buffett era. While Buffett remains Chairman and an active participant in major decisions, Abel is now firmly at the operational helm. His actions are being closely watched as indicators of his leadership style and commitment to the "Berkshire Way." By executing a value-driven buyback and making a substantial personal investment, Abel is not just managing capital; he is managing expectations and cementing trust. He is demonstrating that the disciplined, long-term focus that defined Buffett’s tenure will continue, providing a stable foundation for the conglomerate’s future growth and capital appreciation.

In essence, Berkshire Hathaway’s latest announcements are more than just financial transactions; they are carefully orchestrated signals of confidence, alignment, and continuity, designed to reassure a global investor base navigating the subtle yet significant shift in leadership at one of the world’s most iconic companies.